Factor-adjusted Regularized Model Selection

Team Information

Team Members

Kaizheng Wang, Assistant Professor, Industrial Engineering and Operations Research, School of Engineering and Applied Science, Columbia University

Abstract

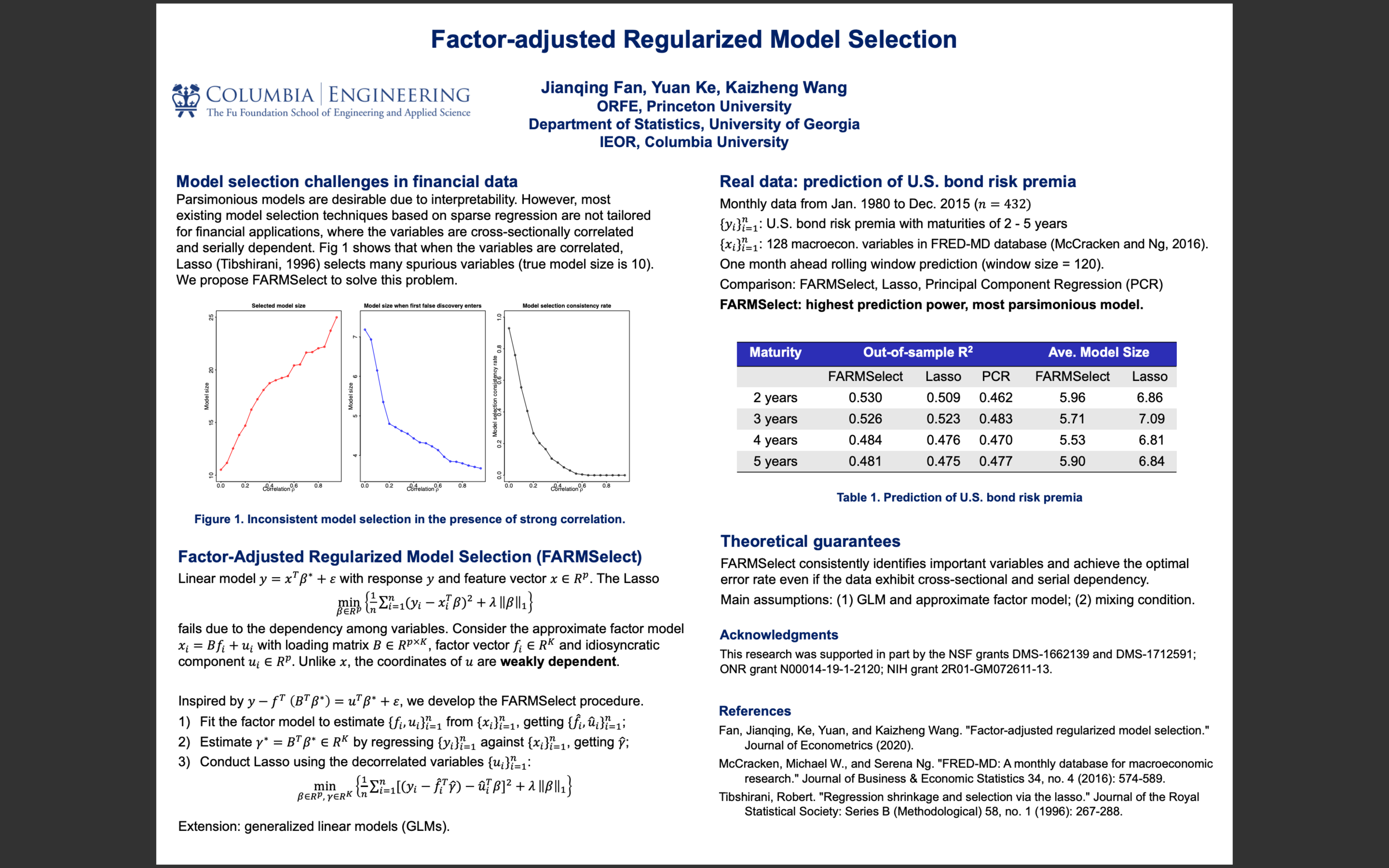

We study model selection consistency for high dimensional sparse regression when the data exhibit both cross-sectional and serial dependency. Motivated by financial studies, we consider the case where covariate dependence can be reduced through the factor model, and propose a consistency strategy named Factor-Adjusted Regularized Model Selection (FARMSelect). We use the U.S. bond risk premium data to demonstrate the nice finite-sample performance in terms of both model selection and out-of-sample prediction.

Contact this Team

Team Contact: Kaizheng Wang (use form to send email)